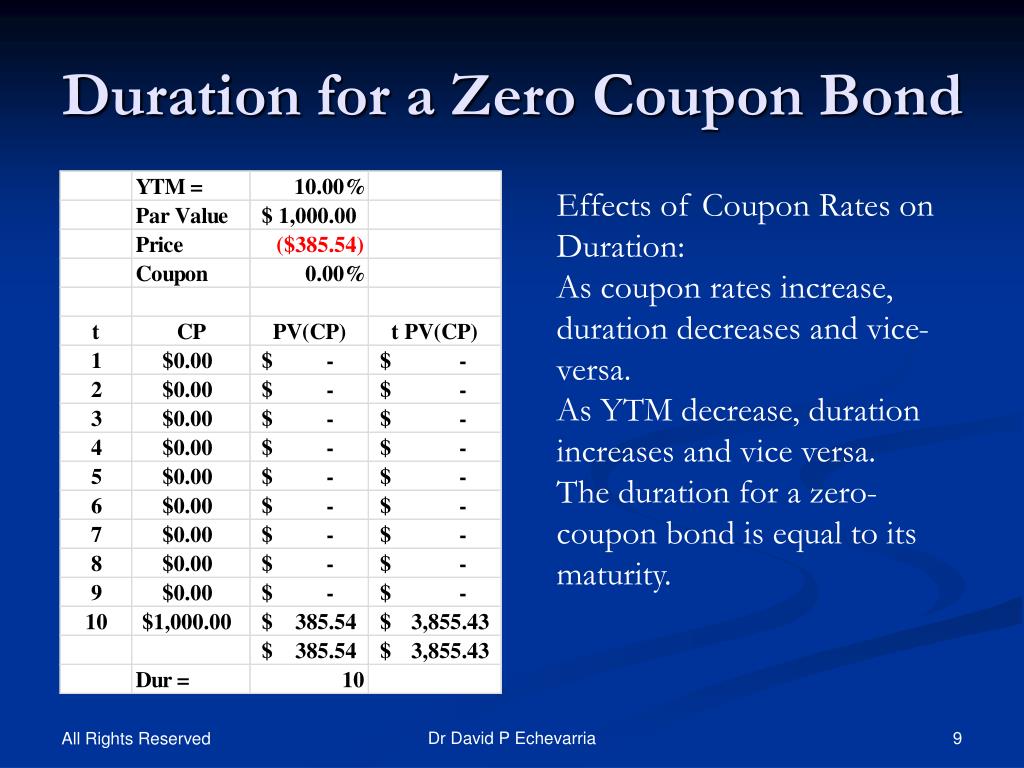

43 duration zero coupon bond

Zero-Coupon Bond: Formula and Excel Calculator U.S. Treasury Bills (or T-Bills) are short-term zero-coupon bonds (< 1 year) issued by the U.S. government. Zero-Coupon Bond Price Formula To calculate the price of a zero-coupon bond - i.e. the present value (PV) - the first step is to find the bond's future value (FV), which is most often $1,000. What Is the Coupon Rate of a Bond? - The Balance Nov 18, 2021 · Another type of bond is a zero coupon bond, which does not pay interest during the time the bond is outstanding. Rather, zero coupon bonds are sold at a discount to their value at maturity. Maturity dates on zero coupon bonds tend to be long term, often not maturing for 10, 15, or more years.

PDF Understanding Duration - BlackRock rates, duration allows for the effective comparison of bonds with different maturities and coupon rates. For example, a 5-year zero coupon bond may be more sensitive to interest rate changes than a 7-year bond with a 6% coupon. By comparing the bonds' durations, you may be able to anticipate the degree of

Duration zero coupon bond

Zero Coupon Bond Calculator – What is the Market Price? - DQYDJ Duration of a bond is a length of time representing how sensitive a bond is to changes in interest rates. Since zero coupon bonds have an equal duration and maturity, interest rate changes have more effect on zero coupon bonds than regular bonds maturity at the same time. (Whether that's good or bad is up to you!) What is the modified duration of a zero coupon bond? Zero coupon bond can be of any duration, can be from one year to 10 years. It is ordinarily from 3 to 5 years. It is ordinarily from 3 to 5 years. Zero coupon bonds are issued at a discount with par value paid on redemption, sometimes with a nominal premium. How to Calculate a Zero Coupon Bond Price - Double Entry Bookkeeping The zero coupon bond price is calculated as follows: n = 3 i = 7% FV = Face value of the bond = 1,000 Zero coupon bond price = FV / (1 + i) n Zero coupon bond price = 1,000 / (1 + 7%) 3 Zero coupon bond price = 816.30 (rounded to 816) The present value of the cash flow from the bond is 816, this is what the investor should be prepared to pay ...

Duration zero coupon bond. Macaulay's Duration | Formula | Example - XPLAIND.com Duration of Bond A is 4.5, i.e. the maturity period (in years) of the zero-coupon bond. Duration of Bond B is calculated by first finding the present value of each of the annual coupons and maturity value. Annual coupon is $50 (i.e. 5% of the $1,000) and the maturity value is $1,000. Convexity of a Bond | Formula | Duration | Calculation The number of coupon flows (cash flows) change the duration and hence the convexity of the bond. The duration of a zero bond is equal to its time to maturity, but as there still exists a convex relationship between its price and yield, zero-coupon bonds have the highest convexity and its prices most sensitive to changes in yield. Chapter 11 - Managing Bond Portfolio Flashcards | Quizlet Bond H and Bond L are zero-coupon bonds that have 10-years remaining until maturity, but Bond H has a higher yield to maturity than Bond L. Bond H's duration is _____ Bond L's duration. When the yields of both bonds increase by 50 basis points, the percentage drop in bond price will be _____. What is the duration of a zero coupon bond? - Quora Zero coupon bond can be of any duration , can be from one year to 10 years. It is ordinarily from 3 to 5 years. Zero coupon bonds are issued at a discount with par value paid on redemption, sometimes with a nominal premium.

Macaulay Duration - Overview, How To Calculate, Factors A zero-coupon bond assumes the highest Macaulay duration compared with coupon bonds, assuming other features are the same. It is equal to the maturity for a zero-coupon bond and is less than the maturity for coupon bonds. Macaulay duration also demonstrates an inverse relationship with yield to maturity. Zero Coupon Bond Calculator - MiniWebtool Zero Coupon Bond Definition A zero-coupon bond is a bond bought at a price lower than its face value, with the face value repaid at the time of maturity. It does not make periodic interest payments. When the bond reaches maturity, its investor receives its face value. It is also called a discount bond or deep discount bond. Formula How to Calculate the Bond Duration (example included) Therefore, for our example, m = 2. Here is a summary of all the components that can be used to calculate Macaulay duration: m = Number of payments per period = 2. YTM = Yield to Maturity = 8% or 0.08. PV = Bond price = 963.7. FV = Bond face value = 1000. C = Coupon rate = 6% or 0.06. Additionally, since the bond matures in 2 years, then for ... Zero-Coupon Bond Definition - Investopedia The maturity dates on zero-coupon bonds are usually long-term, with initial maturities of at least 10 years. These long-term maturity dates let investors plan for long-range goals, such as saving...

Zero Coupon Bond (Definition, Formula, Examples, Calculations) Cube Bank intends to subscribe to a 10-year this Bond having a face value of $1000 per bond. The Yield to Maturity is given as 8%. Accordingly, Zero-Coupon Bond Value = [$1000/ (1+0.08)^10] = $463.19 Thus the Present Value of Zero Coupon Bond with a Yield to maturity of 8% and maturing in 10 years is $463.19. What Is a Zero-Coupon Bond? Definition, Characteristics & Example For instance, if a zero-coupon bond was sold at a $100 discount and matures in four years, its holder would have to pay the applicable bond interest tax rate on $25 worth of the bond's total $100 ... The Macaulay Duration of a Zero-Coupon Bond in Excel Calculating the Macauley Duration in Excel Assume you hold a two-year zero-coupon bond with a par value of $10,000, a yield of 5%, and you want to calculate the duration in Excel. In columns A and... Zero-Coupon Bond - Definition, How It Works, Formula John is looking to purchase a zero-coupon bond with a face value of $1,000 and 5 years to maturity. The interest rate on the bond is 5% compounded annually. What price will John pay for the bond today? Price of bond = $1,000 / (1+0.05) 5 = $783.53 The price that John will pay for the bond today is $783.53. Example 2: Semi-annual Compounding

Zero-coupon bond - PrepNuggets

Modified duration of zero-coupond bond (FRM practice question ... - YouTube A zero-coupon bond with maturity of ten (10) years has a 6% bond-equivalent yield (semi-annual compounding). What is the bond's modified duration?

Zero-Coupon Bond - Assignment Point

问题 1 The modified duration of a zero coupon bond with | Chegg.com Finance questions and answers. 问题 1 The modified duration of a zero coupon bond with a maturity of 4 years and yield to maturity of 5% is 4.2 4.0 3.8 O Cannot be determined. 问题 2 You need to payoff a personal debt in 3 years. The current market interest is 8% and you just purchased a zero-coupon bond that has a duration of 3 years in ...

PPT - CHAPTER 8 PowerPoint Presentation, free download - ID:2104725

Zero Coupon Bond Value - Formula (with Calculator) A 5 year zero coupon bond is issued with a face value of $100 and a rate of 6%. Looking at the formula, $100 would be F, 6% would be r, and t would be 5 years. After solving the equation, the original price or value would be $74.73. After 5 years, the bond could then be redeemed for the $100 face value.

A zero coupon bond d is sold at a deep discount at less than the par ...

Zero Coupon Bond Value Calculator: Calculate Price, Yield to Maturity ... Let's say a zero coupon bond is issued for $500 and will pay $1,000 at maturity in 30 years. Divide the $1,000 by $500 gives us 2. Raise 2 to the 1/30th power and you get 1.02329. Subtract 1, and you have 0.02329, which is 2.3239%. Advantages of Zero-coupon Bonds Most bonds typically pay out a coupon every six months.

1

Modified Duration Definition - Investopedia Feb 12, 2022 · Modified duration is a formula that expresses the measurable change in the value of a security in response to a change in interest rates. Modified duration follows the concept that interest rates ...

Macaulay's Duration, a Second Look - GlynHolton.com

Zero-coupon bond - Wikipedia A zero coupon bond (also discount bond or deep discount bond) is a bond in which the face value is repaid at the time of maturity. ... A zero coupon bond always has a duration equal to its maturity, and a coupon bond always has a lower duration. Strip bonds are normally available from investment dealers maturing at terms up to 30 years.

PPT - FINC4101 Investment Analysis PowerPoint Presentation, free ...

Zero Coupon Bond | Investor.gov The maturity dates on zero coupon bonds are usually long-term—many don't mature for ten, fifteen, or more years. These long-term maturity dates allow an investor to plan for a long-range goal, such as paying for a child's college education. With the deep discount, an investor can put up a small amount of money that can grow over many years.

Zero Coupon Bond Current Affairs Insight

fixed income - Duration of callable zero coupon bond - Quantitative ... What is the bond duration? A- 10 Years B- 5 Years C- 7.5 Years D- Cannot be determined based on the data given. According to me it should be 10 years as the duration of a zero coupon bond is always equal to its maturity. But I am not getting convinced with my answer because of the callable feature in the question.

PPT - Chapter 12 Bond Prices and the Importance of Duration PowerPoint ...

How to use the Excel DURATION function | Exceljet The weight of each cash flow is determined by dividing the present value of the cash flow by the price. Excel also provides the MDURATION function for calculating modified duration. Example. In the example shown, we want to calculate the duration of a bond with an annual coupon rate of 5% and semi-annual payments.

nØthing specia¡ : Duration

Zero-Coupon Bonds: Definition, Formula, Example, Advantages, and ... In the same manner, for bonds that have a relatively shorter maturity duration, investors do not need to worry about the market fluctuation, since the bond's face value is not contingent on market fluctuations. ... Mr. Tee is looking to purchase a zero-coupon bond that has a face value of $50 and has 5 years till maturity. The interest rate ...

Solved: There Is A Zero Coupon Bond That Sells For $436.64... | Chegg.com

Bond Duration Calculator – Macaulay and Modified ... - DQYDJ From the series, you can see that a zero coupon bond has a duration equal to it's time to maturity – it only pays out at maturity. Example: Compute the Macaulay Duration for a Bond. Let's compute the Macaulay duration for a bond with the following stats: Par Value: $1000; Coupon: 5%; Current Trading Price: $960.27; Yield to Maturity: 6.5% ...

PPT - Chapter 12 Bond Prices and the Importance of Duration PowerPoint ...

Bond duration - Wikipedia For a standard bond, the Macaulay duration will be between 0 and the maturity of the bond. It is equal to the maturity if and only if the bond is a zero-coupon bond . Modified duration, on the other hand, is a mathematical derivative (rate of change) of price and measures the percentage rate of change of price with respect to yield.

Coupon Payment Calculator Excel ~ coupon

PDF Duration - New York University Duration 12 Example: Zero-Rate Dollar Duration of a Coupon Bond The zero-rate dollar duration of $1 par of a T-year bond with coupon rate c is This is the dollar price sensitivity to a parallel shift in the zero yield curve. Example: dollar duration of $1 par of a 1-year 6%-coupon bond: € c 2 [0.5 (1+r 0.5 /2) 2 + 1 (1+r 1 /2) 3 + 1.5 (1+r 1 ...

Essay on Bonds: Types and Valuation | Securities | Financial Management

Duration and Convexity, with Illustrations and Formulas Therefore, Frederick Macaulay reasoned that a better measure of interest rate risk is to consider a coupon bond as a series of zero-coupon bonds, where each payment is a zero-coupon bond weighted by the present value of the payment divided by the bond price. Hence, duration is the effective maturity of a bond, which is why it is measured in ...

PPT - Bond Price Volatility PowerPoint Presentation - ID:159962

duration of zero coupon bonds | Forum | Bionic Turtle With respect to a zero coupon bond, Macaulay duration = maturity, and therefore must be a monotonically increasing function of maturity. On the other hand, DV01 of a zero (or deeply discounted) is not strictly increasing as DV01 = P*D/10,000 and the numerator has offsetting effects. If you'd kindly reference, I can fix? Thanks! Apr 7, 2012 #3 S

3.How to calculate a zero coupon bond and coupon bond price By RStudio ...

Zero Coupon Bond Modified Duration Formula - Bionic Turtle We barely need a calculator to find the modified duration of this 3-year, zero-coupon bond. Its Macaulay duration is 3.0 years such that its modified duration is 2.941 = 3.0/ (1+0.04/2) under semi-annually compounded yield of 4.0%.

Post a Comment for "43 duration zero coupon bond"